NetSuite Inventory Management: Everything You Need to Know

Learning the different types of inventory management that you may want to have in your NetSuite ERP is an important step to any NetSuite implementation when getting to your inventory management processes.

- Date

- April 7, 2026

- Read

- 17 min

Inventory is one of the most valuable assets of the company that owns it. In retail, manufacturing, food service, and other sectors, inputs and finished products represent the essence of the business, and poor inventory management can even compromise the business's long-term growth. At the same time, inventory can be considered a liability (not in the accounting sense).

Keeping a large inventory entails, to some extent, several risks for companies, such as the risk of deterioration, theft, damage, obsolescence, or loss, in the case of perishable products.

For these reasons, inventory management is of great importance to all companies, regardless of their size.

Knowing when to restock certain items, the need for purchase and production, the purchase price, and the sale price is essential for the maintenance of activities, which makes this task, in addition to being complex, very delicate.

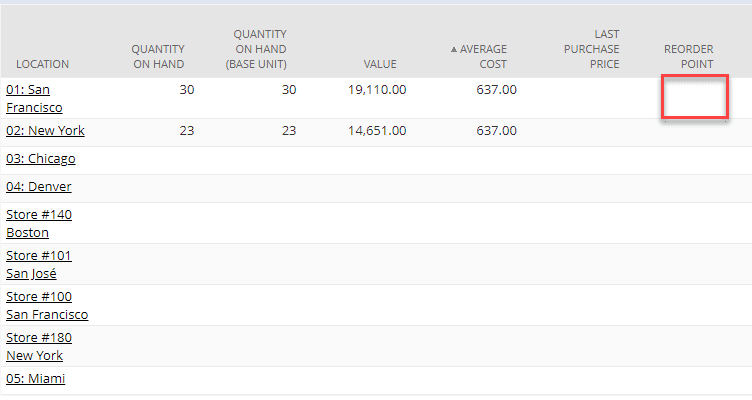

To manage inventories, companies use different tools, such as manual controls, spreadsheets, ERP software, and, more recently, SaaS applications (Software as Service, or software as a service). NetSuite is a great solution for advanced inventory management and allows for automated workflows, reorder points, and various other necessary inventory management tools. This is just a small screenshot of an item record in NetSuite where customers will sometimes select a quantity reorder point.

In this article, the main themes related to inventory management will be addressed, such as its importance, the main mistakes made by companies, how to avoid inventory losses, among others.

What is Inventory Management?

One of the main tasks must be performed in businesses that deal with product inventories, whether raw materials, finished products, or inputs.

Inventory management represents the company's ability to organize and control the quantity of each product at a given time. In addition, it allows the company to understand its product mix and its demands, which in turn will determine purchasing needs.

Another essential point of stock management concerns the valuation of stocks: how much inventory is worth to the company.

Why is Inventory Management Important?

Inventory management is one of the keys to the success of companies, as it aims to ensure the ideal stock for the activity, that is, preventing excess or lack of inventory and ensuring that whenever a customer requests a product, it is provided.

Some experts argue that the ideal is for the inflow and outflow of inventory to be nearly identical.

However, depending on the company's activity, the demands vary significantly during the year, making it necessary for the company to build a safe stock, as running out of stock can dramatically impact its activity.

In addition, companies often obtain advantageous negotiations with their suppliers in case they purchase large quantities. Depending on the situation, it can be a good business opportunity.

Therefore, to make the best decisions for the company, it is necessary to know the activity's operation and the sector's peculiarities so that the company will not suffer either from the excess or the lack of products and goods.

This is only possible with good inventory management.

In addition to enabling the company to make the best decisions, inventory management prevents it from making mistakes, such as buying unnecessary items because they have an attractive price.

Primary Methods of Inventory management

There are different methods of managing stocks. Learn a little more about five more traditional types of inventory management.

FIFO

This methodology follows the principle that the oldest goods in stock are the ones that must be sold first, preventing the items from becoming obsolete. Hence the use of the acronym FIFO, which means "first-in, first-out."

It is one of the inventory management methods most used by companies today. With the constant increase in the prices of stock items, this model tends to value the stock at the closest value to that practiced in the market since it will be composed of the most recently acquired things.

LIFO

LIFO is the opposite of the previous methodology. Its acronym means "last-in, first-out." In this way, the product most recently incorporated into the company's stock is the first one that must be made available for sales.

This inventory control method is not recommended for companies that work with perishable products. They require even more elaborate control methods to not suffer from damage and loss of products.

Since the costs of goods sold are calculated based on the value of the newest products, this methodology makes the accounting profit of companies lower and, therefore, this practice is prohibited by the Internal Revenue Service for purposes of calculating the Income Tax. be used only for managerial purposes.

Average Cost

Also called Moving Weighted Average, this method refreshes inventory values each time a new entry of items is entered by calculating a weighted average.

The average is the result of the sum of the values of old products with the importance of new products, divided by the total quantity of items available in stock.

This method is ideal for companies whose stock item values do not fluctuate widely. Even so, additional controls need to be put in place to verify that inventory is not over or undervalued.

It is worth remembering that Average Cost and PEPS are the only inventory management methods accepted by the Ministry of Finance for Income Tax calculation purposes.

Just in Time

The Just in Time (literally translated as "at the moment") is a management method developed to promote cost reduction. The stock level is maintained at the lowest level, capable of meeting the company's demands.

This methodology requires strict monitoring by managers to prevent the company from missing out on good sales opportunities for not having sufficient stock of products to meet demands. This is one of the leading "sins" committed in inventory management.

For this method to work, it is necessary to have suitable suppliers as partners to meet requests with agility and as often as needed.

ABC Curve

This management method is based on three fundamental pillars to establish the importance of keeping each product in stock. They are turnover, revenue, and profitability.

According to these criteria, inventory items are classified into three types:

- Type A items: these are the most important and most valuable goods. It is necessary to have absolute control, as these are the most valuable items for the company, although they may not be the most numerous. These are products with good turnover but which generate high profitability and revenue.

- Type B items: are medium value goods and, therefore, controls as strict as those classified as A are not used. However, it is necessary to control, mainly, the quantity of these items in stock, as they tend to be the most numerous.

- Type C items: are the least valuable to the company, so it's not that important to adopt too many controls. These items can often be excluded from rotating inventories, for example. They must be kept in small quantities in stock to ensure that any demands are met.

Small Business Inventory Management: Best Practices

Good inventory management is a somewhat complex task as many issues must be analyzed, and controls must be implemented. However, the benefits are many, especially for small businesses, with greater efficiency and, consequently, profitability. Check out some good practices to be implemented:

1. Carry Out Inventories

The first step is crucial. You must physically collect all items in your inventory through an inventory. During this procedure, it is essential that you take the opportunity to organize the arrangement of your products. Separate them by type, each in a specific location. This mapping improves the movement of goods in stock and makes different processes more agile.

How to Record Inventory Data?

There are different ways to compile inventory data. The most common are:

- Manually using pencil/pen and paper

- Using electronic spreadsheets

- With an inventory management system like NetSuite

Although the last option requires investment, in the long run, it will make your company much more agile and competitive, with much more elaborate and adequate controls.

2. Highlight All Important Information

Whichever way you choose to compile your inventory information, it is crucial to establish the relevant information to be collected. If you are unable to record information accurately, you could make incorrect decisions that negatively impact the financial health of your business.

Each inventory item has a large amount of information that can be relevant for decision-making. Among the main ones, the following stand out:

- Reference number or asset control number

- Cost

- Manufacturer

- Category

- Location

- Validity

In addition, vendor-specific information such as the order number and any other criteria useful for your business (color, size, model, etc.) can be included.

To fully understand your stock, it is necessary to know how the merchandise moves, and this implies monitoring the life cycle of each item, from the supplier's purchase date to the sale dates, as well as the cost and price of sale.

3. Pay Attention to Costs and Revenues

Inventory management is not just limited to physical control. For the business to be successful, it is necessary to monitor the stock taking into account the value of its products and its turnover and profit margin.

To manage inventory in this way, it is necessary to know which product sells the most and which generates the most significant profits. For this, you need to consider the selling price (including any discounts applied) of your items.

More complete management systems integrate purchase and sales management, enabling greater precision in your inventory control.

With this information, you will be able to:

- Focus on the most profitable products

- Know the products with the highest and worst performance by quantity and by margin

- Better manage your discounts with accurate item cost information

4. Manage Your Inventory With a Single System

Managing your inventory from different systems is a massive waste of time, and it's straightforward to make mistakes. Choosing a single system to track your inventories will make everything so much easier.

A centralized inventory management system will allow you to:

- Centralize your information and automate processes

- Reduce errors

- Track the entire movement of stock items, from entry to the sale

- Control the inputs used in the production of your products

- Monitor inventory levels

5. Monitor Your Sales, So You Never Run Out of Merchandise

Of all the problems stores can encounter, running out of stock is one of the most dangerous. Monitoring sales is a vital strategy for business growth, not just for controlling inventory.

Based on this information, you can better forecast your purchasing needs and ensure that the company has ordered enough for a certain period by analyzing its sales history and considering the growth projections for the economy and the sector in which it operates.

Review your main products. Are they selling faster than expected? You may have to make a particular order. Are they selling less than expected? You may have to offer discounts or different payment terms to keep the item out of stock.

6. Manage Your Old Goods

Administering old stock correctly will help you avoid losing goods due to obsolescence or expiration and help the company incur losses.

Analyzing items with a downward movement in stock is also an excellent strategy to avoid excess production or even develop strategies to increase product turnover.

With a proper stock management system and following the best practices above, you will keep your stock up to date and, consequently, your customers satisfied with the availability of the products.

Major Mistakes in Inventory Management

Due to the complexity of the activity, errors in inventory management are common. Find out which are the main ones and how to avoid them:

Excess Inventory

Excess inventory is one of the biggest problems faced by companies, especially in times of crisis. When it comes to perishable products, the problem translates into total losses.

In any case, it is still an unnecessary expense because the company no longer has liquid capital available for investment and starts to have a stalled investment. Not to mention storage costs.

It is necessary to focus investments on more profitable products that sell better to prevent this from happening. The only way to do this correctly is to start analyzing your sales month by month.

And not just in the current year, but also compared to the same month last year, vacation periods, etc., to identify possible seasonalities.

Insufficient Inventory

When inventory management is not done well, you end up taking several risks. The lack of products, for example, ends up generating losses that you often don't even notice.

This type of situation can lead, for example, to the loss of customer confidence, pegged sales, and future sales.

The lack of stock is as harmful to the company as the excess. Therefore, it is important to have adequate control so that none of the cases will happen.

Seasonality Problems

Are you aware of the fluctuations that occur in your company's demand? The product offer must be adapted to the needs of its customers, in each season and time of year.

You can't buy the same goods when perhaps your customers are going on vacation and aren't thinking about buying them.

The opposite also happens. There are times, usually festive dates, when there is a tremendous increase in demand.

In addition to capturing this information, companies need to plan well so as not to suffer from external problems, such as supplier delays.

Use of Inefficient Inventory Management Tools

Another common problem in inventory management is using inadequate tracking tools.

It is not enough to use solutions to control batches and product series. It is necessary to have tools that are integrated with the purchasing and sales areas and allow you to control the actual value of your stocks.

If you don't have the right tools, you can make a series of bad decisions that will only be identified much later. In many cases, it will be too late to reverse them, and you will see them translated into very high losses or costs.

In addition, automation of inventory control procedures helps to minimize time and operating costs.

Lack of Physical Inventory

Many companies end up not carrying out inventories regularly and believe that the amount shown in their controls is absolute. This can lead to unnecessary purchasing problems or being out of stock at crucial times for the company.

Inventory Losses, How to Avoid it?

First of all, you need to take into account the leading causes of inventory losses:

Customer Theft

Theft by customers is one of the leading causes of losses in stores, for example. In this sense, it is essential that the company adopt anti-theft systems, keep them in good condition, and place alarms on the products to avoid their deactivation.

In addition, it is necessary to pay attention to areas more prone to theft, such as gondolas.

Internal Employee Theft

The team is also one of the causes of unknown losses in retail companies, whether through the theft of products or the granting of abusive discounts, with the help of employees responsible for sales. Both occurrences, without a doubt, reduce the profitability of the business.

Administrative Errors

Wrong merchandise postings can cause a large amount of loss, just as incorrect pricing also increases the loss of profitability.

If possible, any movement of products in stock needs to be correctly reflected in the management system, integrating with the purchasing procedure to avoid errors.

Errors in Receiving Goods

Suppliers may deliver incorrect products or in lesser quantities than what was purchased. In this sense, it is important to stipulate controls in the goods receipt process.

Breakdown or Expiration of products

Improperly storing products, causing damage, or not controlling perishable products are also frequent causes of loss of merchandise.

Best Ways to Avoid Inventory Losses

1. Investment in Inventory Management

To get a clear idea of what's going on with your products and your sales, you need to manage your inventory. Good software will track products more reliably, from inventory entry to purchase.

In addition, it will allow you to see where discrepancies are occurring and thus get some clues as to which areas to investigate first.

2. Identify Which Products Cause the Most Significant Discrepancies

This can involve several controls, such as changing the product location, limiting access, etc.

3. Install Security Solutions

Security elements, such as cameras or alarms, are a deterrent to potential thieves, in addition to facilitating the monitoring of possible thefts, both by customers and employees.

4. Control Receipts

Taking care of possible inventory losses begins when suppliers deliver their products to the company. At this point, important information such as quantity, validity, and state of conservation of the returned goods must already be observed and registered.

Based on this data, the inventory control teams will be able to make the best decisions to store, distribute and display the purchased items, helping to avoid possible losses.

5. Validity Control

Perishable products need to have strict control over their validity. In this sense, it is often convenient to sell products with a reduced profit margin instead of losing them in stock. In addition, it is necessary to adapt production to demand to avoid excess inventory of these products.

6. Take Inventory Periodically

Regularly inventorying the stock is essential to consolidate physical information (the stock itself) with the virtual databases of stock data, such as the company's management systems (ERP, BI, others).

Regular inventory control is the primary prevention tool against unknown losses, such as theft and misplaced goods.

Detecting and documenting these occurrences can help in the stock safety strategy, which should also be among the managers' concerns.

7. Educate Employees

Inform employees of the consequences of wrongdoing and train them to help them proceed with their tasks, such as placing orders, receiving them, storing them properly.

At the same time, it is necessary to educate them to monitor specific suspicious behavior, know what to do when theft occurs, etc.

Also, establish a corporate culture based on solid values.

Inventory Control Worksheet x Inventory Control System

The control spreadsheets inventory is still widely used by businesses, especially for those small. Among its main advantages, this tool's low cost and popularity stand out, which means that almost all employees can use it.

However, this tool was not designed for managerial purposes and, therefore, it has a series of limitations and, to a certain extent, can contribute to managers making inappropriate decisions.

See some limitations of using spreadsheets in inventory control:

INFORMATION IS ENTERED MANUALLY

Almost all information entered in stock control spreadsheets is done manually, significantly increasing the probability of errors of the most diverse types. They can be typing errors, insertion of duplicate data, or even lack of registration.

FORMULA ERRORS

Many control sheets end up "pulling" information from other sheets. If there is any undue change, or if the spreadsheet is deleted, the company may use incorrect information in its analyses, which can cause significant damage.

MULTIPLE USERS

Often more than one employee can handle inventory control sheets. This practice can result in several problems, as employees without knowledge of how the tool works can end up making undue changes, causing mistakes, and wasting time retrieving the correct information.

MANY VERSIONS

Another problem found is that, often, there are several versions of the same spreadsheet, and an employee may insert new information in the version that is not the most up-to-date, causing data loss and conflicts.

LACK OF INTEGRATION WITH OTHER AREAS

As we have seen, only physical inventory control is insufficient for good inventory management. The information must be integrated for the right decisions, especially with the purchasing and sales areas. Such integration becomes very difficult with the use of spreadsheets.

Using Management Software

On the other hand, stock control through software makes the activity much more flexible, safe, dynamic, and agile. Using a quality system, you can quickly know the value of your inventory at the purchase or sale price and know how well a product is selling.

With inventory control software, you will know which items you need to buy, how much of each product you have, and integrate with information from the purchasing and sales areas, which gives more excellent reliability to the process.

Inventory management will always be a challenge, whether through spreadsheets or software, as many variables interfere with this activity.

Inventory management software explicitly does automated key processes helping you make smarter decisions, increasing efficiency, data reliability, and profits.

Related Articles

- Locked Inventory Items in NetSuite

- How to Fix NetSuite Inventory With a $0 Value

- Troubleshooting NetSuite Sales & Inventory KPIs | Custom GL

- Correcting Count Errors (NetSuite Physical Inventory Count)

- RF-SMART

- Enable Advanced Inventory in NetSuite

Evaluating NetSuite for Inventory Management?

Anchor Group specializes in implementing NetSuite and other NetSuite modules including advanced inventory management. Make sure to contact our team for a discovery call to see if NetSuite is a good fit for you.